|

| |

This

section answers your basic questions about CCAvenue. This

page is primarily intended for existing Sub-Merchants who

have technical questions about CCAvenue. For new client information,

we suggest you start with the 'Why CCAvenue?' Section for

a better introduction to our services. This

section answers your basic questions about CCAvenue. This

page is primarily intended for existing Sub-Merchants who

have technical questions about CCAvenue. For new client information,

we suggest you start with the 'Why CCAvenue?' Section for

a better introduction to our services.

|

|

About

CCAvenue as a payment gateway

|

|

Advantages of CCAvenue to you as a seller

|

|

CCAvenue

convenience for your customers

|

|

Signing

up for a new CCAvenue Account

|

|

Managing

your CCAvenue Account : Export

Procedures and Indian Laws related to Internet Credit Card Sales

|

|

Technical,

Security and other issues

|

|

Billing

in foreign currency on the website

|

|

CCAvenue:

an Online service

|

|

Maintaining

your CCAvenue.com Account

|

About

CCAvenue as a payment gateway

What is CCAvenue?

CCAvenue is a Commerce Service Provider, authorized as a Master

Merchant, by Indian financial institutions, to appoint Sub

Merchants, to accept and validate Internet payments via credit

card, and Net banking facilities from the Sub Merchant's (your)

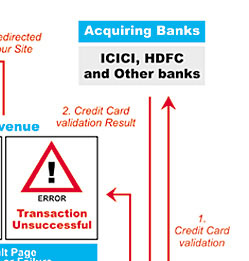

customers in real-time. We provide a secure link between your

website, various credit card issuing institutions, acquiring

Banks and the payment gateway providers. Please Note: At present,

CCAvenue offers these payment services, exclusively for websites

owned by Indian entities only.

|

|

|

What is a payment gateway?

A payment gateway is a software program integrated to a merchant's

website to transmit transaction data to the credit card /

Net Banking acquirer for authorization and settlement. Merchants

gain the ability to perform real-time credit card authorizations

from a web site over the Internet. Customers can pay for purchases

across the Internet through credit cards within seconds, after

the gateway obtains authorization from the credit card institutions.

|

|

|

What does CCavenue do?

CCAvenue provides complete, simple and secure online

payment gateway services and e-business solutions to Indian

websites, with real time credit card and Net Banking transaction

validation. This enables the websites to transact and accept

payments online and in real time.

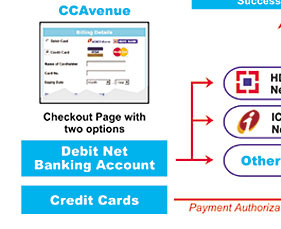

What

are the types of web / integration interfaces offered by

CCAvenue? Does my customer get to see pages which have the

look and feel of my website?

CCAvenue

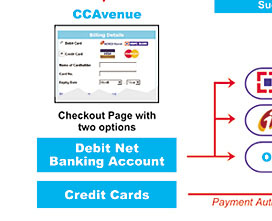

offers you (the Sub Merchant) two interfaces to choose from:

Variable Amount Interface and Shopping Cart Interface. These

interfaces can be seamlessly integrated with your Site.

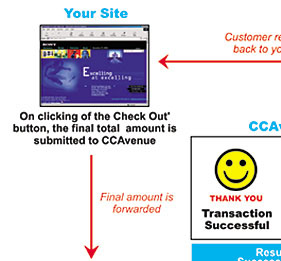

a) Variable Amount Interface : Use this interface

if you have already developed your shopping cart and you

need CCAvenue.com exclusively for final amount authorization.

The customer finishes shopping on your site; and you just

forward the final amount to the CCAvenue 'secure server

final payment check out' page. Your customer then enters

his/her credit card or Net Banking selection and shipping

information to complete the sale. The full transaction flow

from your site to the CCAvenue site to the payment gateway

is explained in detail through the following formats:- flash,

demolink

, livelink)

& flowchart (below)

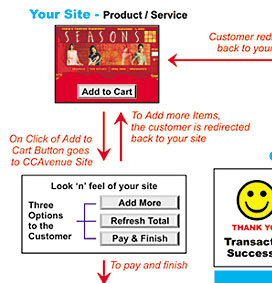

b) Shopping Cart Interface :If you have not yet developed

a shopping cart for your website or you do not want to spend

your precious resources on designing one, then this interface

is just right for you. Use the readymade Shopping cart provided

by CCAvenue; which can be customised to match the look and

feel of your site. At the top of the shopping cart, simply

put up your industry standard 468 x 68 banner, customize the

background colour to match that of your website, add the links

and give it a total look and feel of continuity of your site.

On your site, list your product or services and insert an

'Add To Cart' button next to this list. CCAvenue provides

these buttons along with snippets of HTML code. Once your

customer clicks on the 'Add to Cart' button, he is seamlessly

taken to your customised Shopping Cart hosted on CCAvenue's

secure server. Here he has the option of paying up and finishing

the transaction OR adding more items from your site. Customers

can select products for purchase and add them to a virtual

"Shopping Cart" on CCAvenue secure server. When he has finished

shopping, the customer clicks the 'Checkout' button, enters

his/her credit card and shipping information to complete the

sale. The full transaction flow from your site to the CCAvenue

site to the payment gateway is explained in detail through

the following formats:- flash,

demolink,livelink

& flowchart (below).

|

|

|

Advantages

of CCAvenue to you as a seller

Why Should I Choose CCavenue?

Whatever the size of your e-business, CCAvenue has a solution

for you. The CCAvenue system is flexible enough to suit your

requirements. To provide you and your customers a secure shopping

environment, CCAvenue offers the highest level of SSL encryption.

Precise merchant id's selected by you are used throughout

the system to ensure that transactions arriving at a gateway

are from an identifiable merchant, and that any information

passed back to the merchant is from a CCAvenue gateway.

|

|

|

|

What are the advantages of CCAvenue payment gateway to

me as a Sub-merchant?

CCAvenue offers you the following benefits regardless

of the size of your e-business: Secure links between your

Customer, your site, CCAvenue Payment Gateway and the Acquiring

Banks and also secure links between your customer, CCAvenue

and various National and International banks offering Net-banking

facilities. No merchant account required. Your Indian customers

pay in Indian Rupees. (And not from their forex allowance

of US$ 5,000/- if you billed them through a foreign payment

gateway)Fast and efficient Set Up. (You can go live from sign-up

to first transaction in 4 days.) Fast and efficient credit

card processing (entire process takes less than 15 seconds)

Powerful and informative range of real-time reports Weekly

settlement of your payments, accompanied by a host of value

added features (link) Integrates with any kind of shopping

cart. Credit cards bearing - "Valid in India & Nepal only"

also processed. According to a recent survey, 70% of the credit

cards issued in India are still not accepted by foreign Payment

Gateway Service Providers, as these cards are not globally

valid. As a sub-merchant on CCAvenue, you can now accept these

credit cards along with the globally valid cards of your international

customers. Up-to-date technology: CCAvenue services are constantly

upgraded and updated with cutting edge technology and hence

there is no need for you to upgrade any of your hardware or

software. Just by being a CCAvenue merchant, you automatically

benefit from these advancements. (To See our cost effectiveness

as comparred to other service providers, clickon the following

link for the comparative analysis)

|

|

|

CCAvenue

convenience for your customers

|

CCAvenue convenience for your customers.

- Which

credit cards and Net Banking facilities can my customers

use to purchase on my web site? Does CCAvenue offer a

fail-safe back-up redundancy for Visa & MasterCard processing?

-

Any MASTERCARD, VISA, JCB, Diners Club, Citibank E-cards

and AMERICAN EXPRESS credit cards issued anywhere in the

world. HDFC Bank, Citibank, Centurion Bank, ICICI Infinity,

IDBI and UTI Bank net banking clients can now also pay

you online. CCAvenue will also shortly offer Federal Bank

and Global Trust Bank net banking facilities as a debit

payment option, for your customers. CCAvenue is the worlds'

first and only payment gateway solutions provider to offer

such a wide bouquet of debit options, through the online

net banking interface. Visa

& MasterCard being the more popular online cards, CCAvenue

ensures that at any given time there is always at least

one gateway available to process them. Integrating with

two distinctly separate banks for simultaneously processing

these credit cards transactions i.e. Citibank N.A. and

ICICI Bank Ltd, ensures such an availability. This is

a feature not available with any payment gateway solution

provider elsewhere in the asian region.

|

|

|

Signing

up for a new CCAvenue Account

How long will it take for my application to be processed?

What is the procedure followed by CCAvenue after I sign up?

What is the minimum balance I have to maintain in my CCAvenue

account?

After you sign up online, our internal business and security

team scrutinize your application. This takes about 24 - 48

hrs. On approval, you will receive an e-mail from CCAvenue

containing the good news and a link to CCAvenue's payment

page from where you can pay CCAvenue's set-up fees either

by credit card or demand draft or even a local / at par cheque.

The approval email will also contain a list of documents required

by us to validate your business. You will also have to download

the CCAvenue Client Agreement

, print it out Rs. 100/- stamp paper, get it signed by Authorized

personnel of your firm/company and courier/hand deliver it

to AVENUES (INDIA) PVT. LTD., Plaza Asiad, Second Floor, Santa

Cruz (West), Mumbai 400054, India. We expect that you would

complete all of this procedure within seven days of receipt

of formal approval from us. Your account with CCAvenue will

only be activated on receipt of all of the above. Email notice

of activation of the account will be set to the registered

email address. Merchants can go live within 4 days of sign-up

should they so desire. CCAvenue follows a policy akin to a

bank account. We pay-out all funds over the first Rs 1,000

accumulated into your sub-merchant account. We expect you

to maintain a minimum balance of Rs 1,000/- to keep your account

going. On closure of the account with us this amount is refundable

after 180 days of the last transaction, as this is the period

for which a sub-merchant is liable for chargebacks for Internet

related credit card transactions.

|

|

|

What does CCAvenue facilities cost me? Are there any

hidden charges?

Unlike financial institutions that demand huge upfront fees

and lien deposits CCAvenue's charges are affordable for

all types of business.

For Sub-Merchants with an established e-commerce presence

or those confident of a huge volume we recommend our premium

account. This is available for a one-time setup fee of Rs.

20,000 (to be paid at the time of registering) and an annual

software upgradation charge of Rs 2400/- (at the begining

of every financial year 01 April subsequently).

The transaction discount rate on a credit card transaction

is 5% per transaction, with no minimum or maximum transaction

value or monthly guaranteed volume. (Which means that for

each transaction of Rs 100/- of gross value processed on

your behalf by CCAvenue, you will receive Rs 95/- as payment

in hand)

The transaction discount rate for a net-banking debit transaction

is 4% per transaction, with no minimum or maximum transaction

value or monthly guaranteed volume. (Which means that for

each transaction of Rs 100/- of gross value processed on

your behalf by CCAvenue, you will receive Rs 96/- as payment

in hand)

For

Sub-Merchants with a new e-commerce presence or those just

"testing the waters" we recommend our economy account. This

is available for a one-time setup fee of Rs. 5,000 (to be

paid at the time of registering) and an annual software

upgradation charge of Rs 1,200/- (at the beginning of every

financial year 01 April subsequently).

The transaction discount rate on a credit card transaction

is 7% per transaction, with no minimum or maximum transaction

value or monthly guaranteed volume. (Which means that for

each transaction of Rs 100/- of gross value processed on

your behalf by CCAvenue, you will receive Rs 93/- as payment

in hand)

The transaction discount rate for a net-banking debit transaction

is 4% per transaction, with no minimum or maximum transaction

value or monthly guaranteed volume. (Which means that for

each transaction of Rs 100/- of gross value processed on

your behalf by CCAvenue, you will receive Rs 96/- as payment

in hand)

|

|

|

Managing

your CCAvenue Account :

Export

Procedures and Indian Laws related to Internet Credit Card Sales

Is

it possible to change the "Pay To" details and upgrade the

"Account Type" from Economy to Premium?

In order to change "Pay to" details, you have to mail the

administrator of CCAvenue via the "Help Desk" interface available

on the website. You will receive a mail from the administrator

as soon as the new "Pay to" details are approved. You have

to sign a new agreement for the new "pay to" detail, to take

effect. In order to change the "Account type", a Merchant

may change/upgrade only from economy to premium type (by paying

the up gradation fee of INR 15,000) and not vice-versa. The

new account settings will reflect as soon as the excess fee

payment is cleared and will be applicable from the next weekly

payment cycle. The Sub Merchant does not have to make any

changes on his site for the new settings to take place.

|

|

|

Is it possible to sell my product and service in more

than one currency? How is the charge reflected in my customers'

credit card statement? Does CCAvenue issue me a F.I.R.C

(Foreign Inward Remittance Certificate) for all my overseas

sales?

You

may represent your product pricing in any number of currencies.

At the end of the transaction when your client has to checkout

to the CCAvenue payment option page, we require that the

payment amount is in INR equivalent only. This is because

we do not process the final payment in any other currency

but INR as we are subject to such RBI rules and Regulations.

You need not create a different set of shopping cart links.

Example:

Let us assume you are keen to sell a product at US$ 10/-

to a prospective US customer and feel that it is an attractive

price for your product. So you represent US$ 10 on your

web page. When the customer completes his shopping and the

data of your shopping cart is to be sent to the CCavenue

pay page you need to ensure that you have converted this

amount to INR.

What benchmark to use? No genius in the world can predict

at what exchange rate (INR >< US$) rate the end customer

is going to get his credit card bill as this fluctuates

by the minute. So to play safe ensure that no matter what

happens the end customer should not see any amount over

US$ 10/- on his credit card billing statement.

How

does one do this?

Lets

say the US$ rate today for INR is INR 48.50 = US$ 1. You

should take a benchmark of INR 48.0 = US$ 1. Which means

that even if the clients' bank is actually using the exchange

rate INR is INR 48.50 = US$ 1 the client will only be billed

US$ 9.89 / and not the US$ 10/- which he agreed to pay you.

(This is arrived at by US$ 10 x 48.0 = INR 480 / 48.5 =

9.89)

Off course you will have to constantly monitor that INR

>< US$ rate of exchange and ensure that at any given time

the difference parameter is maintained. However one great

factor which works in your favor constantly is the fact

that the US$ is constantly appreciating against the INR

so even if you do not change or monitor your differential

factor for small changes you will still land up charging

the customer a little lesser in US$ than that he was shown

the bill for. However you must also ensure that you do not

under price yourself on the exchange rate too much and do

upwardly revise your INR calculation if there is a huge

jump in the exchange rates, so that this jump can add to

your profitability.

Therefore when you throw the final amount of your shopping

cart onto the CCavenue pay page, you need to convert this

amount at a fixed rate into INR and throw the INR amount

only. Your buyer from outside India will see the INR amount

on this CCAvenue page (which offers multiple payment options).

He will also be told that if he wants to view this INR amount

in his local currency he could also use the live CCAvenue

currency converter link. This would show him the approximate

amount in his local currency, which would be billed to his

credit card statement at the time of that precise particular

transaction. Your customer will be billed in his local currency

in his card statement.

RBI insists that Merchants in India settle transactions

in INR only and the respective banks give a foreign exchange

inward remittance certificate (F.I.R.C.), which we (CCAvenue)

then pass on to you (Our Sub Merchant). This takes care

of the Income Tax part of things, to enable you to claim

exports benefits under section 80 HH of the Income Tax Act.

CCAvenue will issue you a FIRC (Foreign Inward Remittance

Certificate) for all overseas transactions done. This will

be issued on a quarterly basis. A small documentation fee

may be levied.

|

|

|

What is the export procedure related to Internet sales?

Basically the transactions received over the Internet can

be divided into the following classes.

a) Export as Gift Shipment - No SDF or GR is required unto

a value of Rs 1,00,000 (Please download rbi_rules_exports.pdf)

b) Exports in normal course without SDF or GR if the exporter

gives a declaration that the value does not exceed Rs 25,000

per shipment. (Please download rbi_rules_exports.pdf)

Please also download and check out rbi_guidelines_for_export_receipts.pdf,

in which it is stated that credit card, as a means of payment,

is acceptable for export of goods and/ or services.

Also Click

here ,to Download the AP (DIR Sense) Circular No.53

(June 27,2002) Issued by the Reserve Bank of India, regarding

the Use Of Credit Cards.

Courier Export Procedure:

If you have goods on which you intend to claim duty drawback

benefits or import license benefits or any other benefits

that relate to the Ministry of Commerce then it is important

that exports be carried out with an SDF and regular shipping

bills as well as the courier endorsed House Airway Bill which

clearly shows your consignment number marked. All of these

documents should be attested by the customs authorities and

provided to you by the courier company.

Please do also note that for the purpose of claiming export

performance for Income tax benefits under section 80 HHC,

you only need to provide an FIRC certificate, which proves

that the foreign exchange has been earned. This has to be

certified by a CA. CCAvenue will provide you the FIRC( Foreign

Inward Remittance Certificate) for all your transactions which

are through your Non-Indian customers.

|

|

|

Whose name will appear in my customers' credit card statement?

Your customer's credit card statement will be billed as CCAvenue.com

or Avenues (I) Pvt. Ltd. During the transaction and after

successful payment we make it amply evident to your customer

(on the pay page and by a confirmation e-mail) that his credit

card statement will reflect the charge as this.

|

|

|

What is a credit card chargeback? What is CCAvenue's

credit card chargeback policy?

A refund that is forced by a credit cardholder's credit

card company is known as charge back. This occurs when a

cardholder decides to formally dispute a charge on his/her

credit card bill, usually because someone else fraudulently

used that card number.

Credit Cards Permit Chargebacks As per VISA & MASTERCARD

rules any online transaction can/may also be revoked or

refuted by a customer to a Sub Merchant via his card-issuing

bank for the following reasons. This is allowable for up

to 6 months from date of the transaction.

a) The Sub Merchant has not shipped the goods or delivered

the promised service.

b) The Sub Merchant has taken back the goods /cancelled

the services but not yet issued a refund on the credit card.

c) The cardholder's credit card has been fraudulently used

by someone else to procure goods and services - without

knowledge or prior agreement of the cardholder.

CCAvenue's payment gateway service provider, ICICI Bank

and Citibank, have state-of-the-art fraud screening capabilities

to reduce risks. However, if any chargeback is reported

by the cardholder, you (sub-merchant) will be liable to

pay the amount back to CCAvenue or it will be adjusted with

the current balance of your account with CCAvenue; or you

will be liable to refund back the disputed amount back to

CCAvenue. Please note that this practice is universal and

is followed by all payment gateway service providers the

world over. CCAvenue has also an in-house team, which will

screen all the transactions. Please see the section on fraud

reduction tips for more information.

In cases which prima facie look fraudulent, the same will

be referred back to payment gateway for a further thorough

authorization and if it is still authorized then CCAvenue

will forward the transaction to the Sub Merchant so as to

enable him/her to use his/her judgment whether or not he

wants to execute the order or not. The chargeback disputes

are normally less than 1% of the total transactions in a

year.

a) Sub Merchant should keep complete proof of goods being

shipped. This could be in the form of a Courier consignment

note or Receipt from the final consignee.

c) The Sub Merchant can prove that the customer was informed

in advance about refunds / return of goods for replacement

faulty goods.

A CHARGEBACK CAN ONLY BE REVERSED IF THE CREDIT CARD

HOLDER FORMALLY INFORMS HIS/HER BANK OR CREDIT CARD ISSUING

INSTITUTION THAT HE/SHE WILL ACCEPT THE DISPUTED CHARGE.

Fraudulent use of a credit card on the Internet is always

at the risk of the Sub Merchant.

Sub Merchants should keep an internal benchmark for the

level of transaction for which he will take a risk, without

asking for additional documentation from a customer.

Example: ABC Shops has internally set a per transaction

limit of Rs 30,500/-. Which means that up to Rs 30,500/-,

ABC Shops will process an order without asking the customer

to provide additional proof. If the transaction amount is

more than the internal benchmark of Rs. 30,500/- then poof

is required for:

a) That this customer owns the credit card he is using.

b) He is who he says he is. (ID)

So ABC Shops asks any customer who does a transaction

over Rs 30,500 to send by fax the following:-

a) The last statement he received from the credit card company,

which clearly shows his credit card billing address as well

as the credit card number. b) A copy of his driving license

/ national identity card / PAN No. / Passport which proves

he is the person who has placed the order. When ABC Shops

has these documents, then they can go ahead with the customer

without any doubts knowing full well that no fraudulent

usage is taking place of the credit card being used for

the purchase of their goods or service.

|

|

|

|

|

What

is "Authorise and Capture" facility? Why shaould merchants ship

the products within 12 days and capture their order amounts

from their CCAvenue account backend?

Once a transaction of say Rs. 10,000/- comes from your site

and forwarded to the gateway and authorized in real time, it

means that Rs. 10,000/- of your customers credit card is blocked

from his credit card limit that he enjoys for a period of 13

days. For eg. If you customers credit card has a credit limit

of Rs. 40,000/-, Rs. 10,000 will be blocked for your transaction

for a period of 13 days from the time of the transaction from

your site. Your customer after doing transaction from your site,

will have only a credit card limit of Rs. 30,000/- left. This

Rs. 10,000 that is blocked for 13 days will not be reflected

in his credit card statement until unless you capture the order

from your CCAvenue account backend, only after which it will

be reflected in his credit card statement. Therefore you have

to ship your order within 12 days and capture the amounts from

your CCAvenue account backend. If you dont capture within 12

days, the transaction automatically evaporates from the payment

gateway system on the 13th day and the credit card limit of

Rs. 40,000/- is restored to your customers credit card. You

cannot block your customers card forever. This facility helps

Merchants in a way that if they want to cancel or do partial

capture within 12 days of the receipt of the order, then they

do not have to pay any cancellation charges of 5% on the cancelled

amounts. Before the introduction of this facility, merchants

had to pay cancellation charges for orders they could not fullfill.

|

|

|

What are CCAvenue's refund and end customer dispute policies?

CCAvenue maintains a customer-friendly refund policy. This

keeps our administrative costs under control in two ways:

First, it reduces the amount of time spent researching customer

inquiries; and secondly, it reduces the occurrence of chargeback

disputes. (A chargeback dispute is a refund that is forced

by the customer's credit card company.)

Granting Refund to customer:-

In most situations when a customer asks for a refund, we want

to try our best to grant that refund. Here are some guidelines

on our refund and dispute policies: The Seller sets a time

limit: The sub-merchant is required to set the refund time

limit on his/her site depending on the goods sold on his/her

site. If a customer is dissatisfied with a product that he/she

has ordered, the client should accept the product back and

grant a refund. If desired, a client may specify that shipping

charges are not refundable; however we would prefer to refund

the shipping charges as well.

|

|

|

|

|

Can

I cancel an order that I have received from my customer? Will

I be liable to pay any cancellation fees?

A

Sub Merchant can cancel an order with out any Service fees being

charged only as long as the order is cancelled in the window

period (this period is fixed by CCAvenue which is currently

set at twelve days). If the sub merchant fails to either capture/cancel

in the window period, transaction becomes invalid. Note: This

option is not available for payment by Direct Debit cards In

case of debit in ICICI net banking account, a refund will be

made only if the order is cancelled within 10 days, from the

date when the order is placed. |

|

|

|

Technical,

Security and other issues |

|

When is a successful transaction eligible for payment? What

action is required by a sub-merchant to enable CCAvenue to

process a scheduled payout? What payout schedule does CCAvenue

currently follow?

ransactions

processed by credit card through CCAvenue are always presented

to the sub-merchant in the "pending" mode. Which means that

the sub-merchant is guarenteed that the customers card is

good / credit worthy for the amount of that transaction for

the next 12 days. During this period of 12 days the sub-merchant

has to perform any one of the following actions.

a) He may decide not to fulfill the order and mark it as cancelled.

b) After arriving at a consensus with the buyer decide to

ship part of the ordered goods and claim only an amount equal

to the shipped order.

c) Ship all of the ordered goods and claim the entire value

of the transaction.

If the sub-merchant is confident of shipping the goods after

a period of 12 days ( and has the agreement of the customer

for this) he may go ahead and capture the amount, and subsequently

ship the goods as per their agreement. Should the sub-merchant

subsequently fail to do this and wish to refund the amount,

the charge of 7% or 5% will have to be borne for the gateway

usage. Once the capture / fulfillment process has been completed

by the sub-merchant CCAvenue's accounts department will process

all such "captures" undertaken till mid-night of Thursday

and process payments to reach the sub-merchants' account by

direct credit / office by an at par cheque on the following

Monday.

|

|

|

|

|

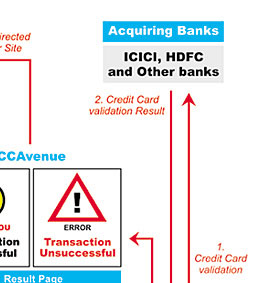

Is CCAvenue more secure than other Payment Service Providers?

Yes

- CCAvenue uses secure servers throughout. Contrary to media

myth, computer-to-computer transactions using secure servers

are generally considered very safe indeed - certainly as safe

as, or even safer than, transactions which rely on signatures

on bits of paper or card details dictated across a potentially

open telephone lines. CCAvenue contains a number of features

designed for e-commerce security across the Internet. Combined,

these features make CCAvenue many times more secure than other

"distant" users of a credit or debit card, such as telephone

or mail order and of course, its competitors. CCAvenue adopts

stringent security measures to ensure that critically sensitive

information, such as your customer's personal information, is

protected. For ultimate data security CCAvenue follows the policy

of making end customers place their credit card numbers and

bank account details directly onto the secure web pages provided

on Payseal.com and citibank.co.in and the various Net Banking

interfaces.

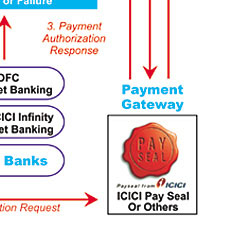

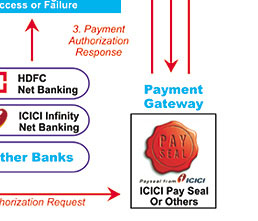

Authorization by ICICI's Payseal and Citibank secure

gateways

All your customers' credit card Authorization is done using

ICICI's E-Payments and Citibank High End Secure Payment Gateways.

Your customers enter all their personal information and credit

card details on ICICI's E-Payments(Payseal) and Citibank's secure

servers and the same is encrypted before it is transmitted over

the Internet to the Acquiring Banks. Additionally CCAvenue's

server is behind security firewalls to ensure maximum protection

of your customer's information. This guarantees that your information

is inaccessible to any third party. CCAvenue uses industry-standard

SSL (Standard Sockets Layer) Technology, which is used worldwide,

for this data encryption.

Authentication by Verisign

CCAvenue is registered with Verisign, the world's best and most

trust worthy Net Authentication Agency. Click

here to verify our certificate. CCAvenue also follows

strict in-house security guidelines for ensuring confidentiality

of your customer information. Since the Payment Gateway application

software is maintained at ICICI's E-Payments and Citibank's

secure high-end servers, new payment technologies, standards

and features are automatically implemented as they emerge. Citibanks

and ICICI's E-Payments payment gateway is integrated with risk

management component, which empowers them with the ability to

control risk effectively. So, without changing your interface,

you get the benefits of the latest technologies, which allows

you to stay ahead in the rapidly changing landscape of E-commerce.

|

|

|

|

|

What level of encryption does CCAvenue use?

CCAvenue uses the most powerful Verisign secure socket layer

(SSL) for encrypting customer data during transmission. To put

this into non-technical terms, it would take 340,000,000,000

years for today's fastest computers to crack Verisign SSL. Click

here to verify our certificate. |

|

|

|

Billing

in foreign currency on the website |

Can

I offer the products on my site with INR as well as USD pricing

while maintaining a single CCAvenue account. If yes, should

I use two different shopping cart links for this purpose?

You may represent your product pricing in any number of currencies.

At the end of the transaction when your client has to check-out

to the CCAvenue payment option page, we require that the payment

amount is in INR equivalent only. This is because we do not

process the final payment in any other currency but INR; because

of RBI rules and Regulations. And no, you do not have to create

a separate shopping cart link for the various currencies. |

|

|

|

|

How

can I ensure that the payment amount reflected on the final

CCAvenue checkout page is in INR equivalent?

You need to have a backend process that will convert your displayed

foreign currency price into INR. Eg. If a customer in the US

buys a product worth US$10, this amount must get converted to

Indian Rupees at the current exchange rate at your end; before

it is thrown to CCAvenue. Your buyer from outside India will

see the INR amount on this CCAvenue page (which offers multiple

payment options). At this point, he can view the exchange value

of the INR amount being billed to him in his local currency;

by using the live CCAvenue currency convertor link. By calculating

the exchange value at the precise time of the transaction, (INR

>< US$)the customer can see exactly how much will be billed

to him in his currency on his credit card statement.

Your customer will be billed in his local currency in his card

statement.

|

Particulars

|

Amount

|

|

Customer

Buy Price

|

5%

US$10

|

|

Live

Conversion rate on the CCAVenue currency convertor

|

US$1

= INR 48.5

|

|

Actual

Amount billable by CCAvenue in INR (US$10 x 48.5)

|

INR 485

|

|

Your

website Conversion rate

|

US$1

= INR 48.0

|

|

Amount

thrown to CCAvenue Payment checkout page(US$10 x 48.0)

|

INR

480

|

|

Amount

billed to, and payable by, customer in US$ according

to your exchange ratio

|

extra

|

|

Amount

Charged to your customer's credit card

|

--INR480

>< US$9.89

|

Please

do a test transaction on a website like www.saranam.com

and see how it works, it will be more clear then. |

|

|

|

With

the exchange rate fluctuating on a daily basis, how can I ensure

a comfortable deal for the customers and myself?

No genius in the world can predict at what exchange rate (INR

>< US$) rate the end customer is going to get his credit card

bill as this fluctuates by the minute. So to play safe, you

must ensure that, no matter what happens, the end customer should

not see any amount over US$10/- on his credit card billing statement.

For this, you need to work with a benchmark. Let's assume, the

US$ rate today for INR is INR 48.50 = US$ 1. You should take

a benchmark of INR 48.0 = US$ 1. Which means that even if the

clients' bank is actually using the exchange rate INR is INR

48.50 = US$1, the client will only be billed US$9.89; as against

US$10/- which he agreed to pay you. (This is arrived at by US$10

x 48.0 = INR 480/48.5 = 9.89) To ensure the best deal for both

you and the customer, you will have to regularly monitor the

INR >< US$ rate of exchange, and maintain an optimum difference

parameter. While small corrections in the exchange rate do not

affect your customer's price negatively, you must also be careful

not to underprice yourself on the exchange rate too much. Do

upwardly revise your INR calculation if there is a huge jump

in the exchange rates, so that this jump can add to your profitability.

|

|

|

|

|

Will

I be able to claim export benefits for all my overseas credit

card transactions?

In what currency will my customer be billed? RBI insists that

Merchants in India settle transactions in INR only and the respective

banks give a foreign exchange inward remittance certificate.

CCAvenue will then pass this certificate on to you, our Sub-Merchant.

This would take care of your Income Tax issues, enabling you

to claim exports benefits under section 80 HH of the Income

Tax Act. |

|

|

| CCAvenue:

an Online service |

Does

CCAvenue have any offline services or support infrastructure?

CCAvenue is a pure internet model with only online sales and

support. All the details you require to enroll and conduct business

through CCAvenue are available at www.ccavenue.com For any specific

queries not by the FAQs, or info on the website, please email

us at service@ccavenue.com. Alternatively you can chat online

with our support staff on any day from Monday to Saturday, between

10.00 am - 6 pm on MSN Messenger. (ccavenue@hotmail.com / ccavenue1@hotmail.com).

|

|

|

| Maintaining

your CCAvenue.com Account |

How

can I check the amount payable to me by CCAvenue?

To confirm your current balance payable, log in to your CCAvenue.com

account by using your user name and password. On the screen

that follows, click "View Account Statement" option. |

|

|

|

Do

I have to maintain any minimum balance in my CCAvenue.com Account?

Yes, just as you are required to maintain a minimum amount in

your savings account in a nationalised bank; you (sub-merchant)

need to maintain a minimum balance of Rs 1000/- in your online

CCAvenue.com Account.(Please refer the clause of 17 in the agreement.)

|

|

|

|

|

How

often will I receive my payouts?

CCAvenue settles payments on a weekly basis. Once the net

payables in your account exceed Rs.1000/-, CCAvenue will issue

regular cheques for all amounts over & above of Rs.1000/-

according to our weekly payment basis. That is, for the transactions

shipped/executed by you till Thursday, you will be paid on

the following Monday.

Your cheques will be couriered every Friday evening via a

PROFESSIONAL Courier and the dispatch details of the same

will be emailed to you the following Monday.

Alternatively, if you have an account in any of the banks

listed below, you cheques can be directly deposited to your

account with same being reflected the next day.

List of banks:

-

HDFC

- ICICI

- CITI

Bank

- HSBC

- Standard

Chartered

- Centurion

Bank.

- IDBI

- Global

Trust Bank

|

Signing

Up

|

|

|

|